Categories

What is provision for credit losses? It’s a financial term that is highly regarded in banking and lending.

Let’s set the stage: Picture yourself as a bank assessing the likelihood of borrowers defaulting on their loans. That is precisely when provision for credit losses becomes relevant.

Provision for credit losses is not just another accounting entry. It represents funds set aside for possible losses on loans that may not be repaid. Understanding the provision for credit losses is essential in an economy heavily dependent on borrowing for development.

In 2020, banks around the globe set aside over $1.28 trillion for credit loss reserves. Why? To address the economic uncertainties triggered by the pandemic. This significant amount highlights this provision’s importance in upholding financial institutions’ stability and resilience.

So, what is provision for credit losses? It is a fundamental element of risk management and financial prudential. Understanding provides stakeholders with insight into the well-being of financial institutions and the overall economy.

This blog post will delve into the intricacies of credit loss provisioning and highlight its importance. We’ll offer insights to help you comprehend the impact of this essential financial safeguard.

First…

Definition: Provision for Credit Losses (PCL) is an accounting expense used by banks and financial institutions to cover potential loan losses. It reflects the estimated amount of loans that might not be repaid. PCL is crucial for assessing a bank’s financial health.

Banks analyze historical data and economic conditions to determine PCL. They consider factors like borrower creditworthiness and market trends. PCL appears on the income statement, reducing net income.

An increase in PCL indicates higher expected loan defaults, signaling potential risks in the loan portfolio. Conversely, a decrease suggests improved loan performance.

PCL ensures banks maintain sufficient reserves. This reserve protects against financial instability.

Accurate PCL calculation is vital for regulatory compliance. It also helps maintain investor confidence and trust.

PCL is a key metric in lenders’ financial risk management.

Provision for credit losses means:

Accounts receivable (AR) are anticipated to be converted into cash within a year or operating cycle. Therefore, they are classified as current assets on a company’s balance sheet. Nonetheless, let’s say a portion of AR is considered uncollectible. This could result in an overstatement of the company’s working capital and stockholders’ equity.

To prevent exaggeration, a company might predict the amount of its accounts receivable that is unlikely to be collected. The approximate amount is recorded in a provision for credit losses contra asset account on the balance sheet. Recordings of increases to the account can also be found in the income statement for uncollectible account expenses.

This entry recognizes the anticipated losses from uncollectible accounts, affecting the company’s profitability. Regularly updating this provision allows the company to account for changing economic conditions and the creditworthiness of its customers.

A company demonstrates prudent financial management by accurately estimating and recording potential credit losses. It aligns its reported assets and earnings with the actual economic value expected to be realized. This practice complies with accounting standards and provides a more transparent view of the company’s financial position to stakeholders.

Provision for credit losses is a crucial component of financial management for banks and financial institutions. It is vital in maintaining these entities’ overall health and stability. Understanding its importance can be categorized into several key areas:

Provision for credit losses and allowance for credit losses are two critical concepts in accounting for financial institutions. Understanding these two terms’ differences is essential for accurate financial analysis and reporting. Here are the key differences between credit losses vs. allowances.

| Aspect | Provision for Credit Losses | Allowance for Credit Losses |

| Definition | An expense recorded on the income statement reflects estimated potential loan losses for a specific period. | A contra-asset account on the balance sheet shows the cumulative amount set aside to cover potential loan losses. |

| Purpose | To recognize and account for anticipated loan losses during a financial period. | To adjust the value of accounts receivable to reflect expected uncollectible amounts. |

| Financial Statement Location | Income statement | Balance sheet |

| Nature | Expense | Contra asset |

| Timing | Recorded periodically (e.g., quarterly or annually) based on loan loss estimates. | Continuously adjusted as loans are written off or recovered. |

| Impact on Financials | Reduces net income | Reduces net accounts receivable |

| Regulatory Requirement | Often required to comply with accounting standards and regulations. | Required to present a true and fair view of financial position. |

| Calculation Basis | Based on historical data, economic conditions, and borrower creditworthiness. | Reflects the aggregate of all provisions made over time, adjusted for actual losses and recoveries. |

PCL’s primary function is to ensure the financial statements accurately reflect an institution’s financial health and risk exposure. It serves multiple critical purposes, which can be categorized as follows:

Data analysis is like solving a puzzle with pieces that keep changing shape. Visualizing data is key, especially when analyzing provision for credit losses. It allows quick insights and patterns to emerge, making complex data more understandable.

However, using Excel for this task can be limiting. Why? It often fails to create impactful visual representations.

This is where ChartExpo comes in as a solution to Excel’s limitations. ChartExpo offers advanced data visualization capabilities, including a Waterfall chart, that effectively convey complex financial data.

Let’s learn how to install ChartExpo in Excel.

ChartExpo charts are available both in Google Sheets and Microsoft Excel. Please use the following CTAs to install the tool of your choice and create beautiful visualizations with a few clicks in your favorite tool.

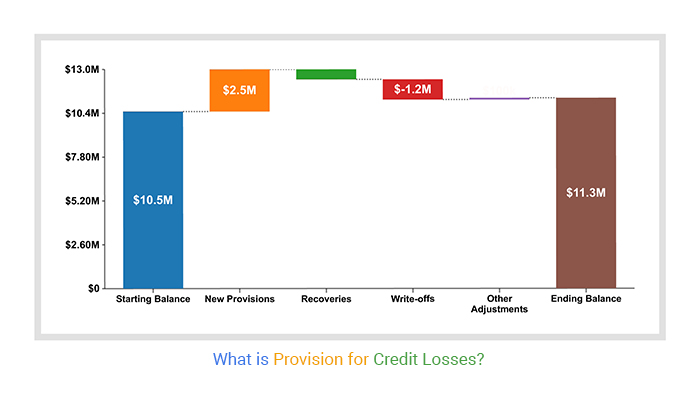

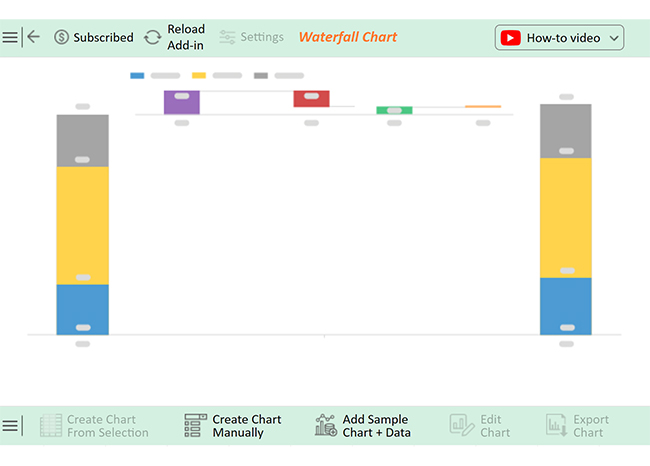

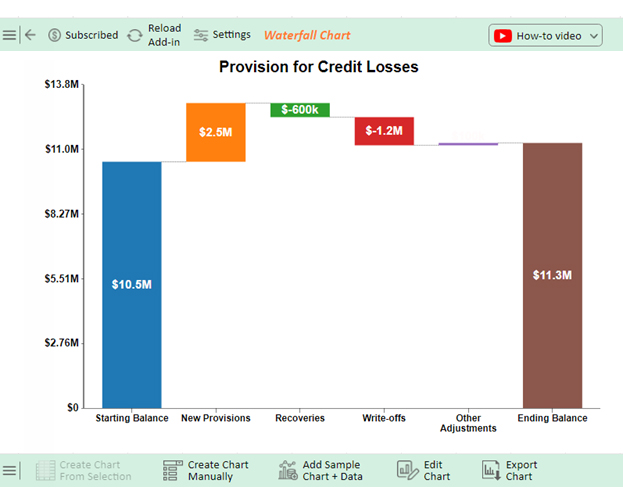

Let’s analyze the provision for credit losses ratio data below using ChartExpo.

| Heads | Amount |

| Starting Balance | 10,500,000 |

| New Provisions | 2,500,000 |

| Recoveries | -600,000 |

| Write-offs | -1,200,000 |

| Other Adjustments | 100,000 |

| Ending Balance | 11,300,000 |

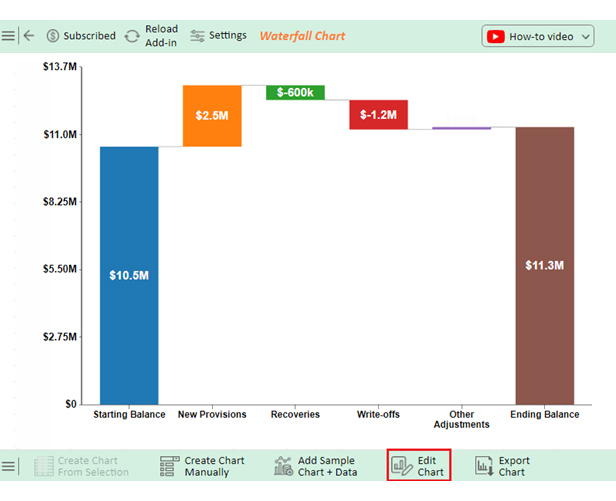

The chart displays the variations in the provision for credit losses over a specific timeframe. The initial amount was $10,500,000. New provisions totaling $2,500,000 were added. The total amount of recoveries from loans that were previously written off was $600,000. Uncollectible loan write-offs amounted to $1,200,000. The provision was raised by an additional $100,000 due to other adjustments. The final amount of the provision for credit losses was $11,300,000.

The chart provides the following key insights:

Effective management of the provision for credit losses (PCL) is essential for lending institutions’ financial health and stability. Proper PCL management ensures potential credit risks are anticipated, quantified, and mitigated. This enhances the institution’s ability to weather economic fluctuations and maintain investor confidence. The following best practices are crucial for robust PCL management:

Banks make provision for credit losses to anticipate potential loan defaults. This helps manage financial risk and ensures stability. It also ensures accurate financial reporting and regulatory compliance and maintains investor confidence. Proper provisions safeguard against unexpected economic downturns.

The expected credit loss (ECL) provision estimates potential loan defaults over a loan’s lifetime. It considers historical data, current conditions, and future forecasts. ECL aims to provide a realistic view of credit risk, ensuring accurate financial reporting and stability.

A negative provision for credit losses means the bank has reduced its previous estimates of potential loan defaults. This indicates improved loan performance or recovery of previously written-off debts, leading to a reversal of excess provisions.

Provision for credit losses (PCL) is an essential financial tool. It helps banks anticipate potential loan defaults and ensures that financial institutions are prepared for credit risks. PCL is recorded as an expense on the income statement.

Banks use historical data and economic forecasts to estimate PCL. They analyze borrower creditworthiness and market conditions. Accurate estimation of PCL is crucial for reflecting the true financial health of the institution. It prevents overstatement of assets and income.

PCL plays a significant role in financial stability. By maintaining adequate provisions, banks can absorb unexpected loan losses. This buffer is vital during economic downturns, ensuring banks remain solvent and operational.

Another key aspect is regulatory compliance. Banks are required to maintain PCL according to accounting standards and regulations. This compliance promotes transparency and trust in the financial system. It reassures investors and stakeholders about the bank’s financial practices.

In summary, provision for credit losses is a proactive measure. It helps manage credit risk, ensures accurate financial reporting, and maintains regulatory compliance. PCL is fundamental for financial stability and investor confidence.

Do not hesitate.

Get started with proper PCL management using ChartExpo today to support sustainable growth and profitability.

How much did you enjoy this article?

Calculate accounts receivable turnover ratio to measure credit collection speed, improve cash flow, and strengthen your financial strategy. Read on!

Change Management KPIs are the key to tracking adoption, performance, and ROI during transitions. Find out which metrics matter. Read on!

Data collection methods and techniques determine the quality of every insight you act on. Explore key approaches for gathering reliable data. Read on!