Categories

What is a medical loss ratio?

Picture this situation: You visit a healthcare provider for care, and later on, your insurance company pays for the expenses. Have you ever considered the portion of your premium allocated toward medical costs?

This is where the medical loss ratio becomes relevant.

What is a medical loss ratio (MLR)? MLR is the portion of premium revenue insurance companies must allocate to healthcare and quality improvement activities. It guarantees that your insurance funds go towards your healthcare benefits rather than just covering administrative expenses and earnings.

Here’s an interesting fact: The ACA requires insurance companies to allocate 80% of premiums towards healthcare and quality enhancement for individual and small group markets. For large group markets, the mandate is 85%. This means that the MLR is a safeguard to prioritize delivering essential health services to policyholders.

So, why is understanding the medical loss ratio important? It explains the effectiveness of your insurance provider in handling premiums to offer optimal healthcare coverage. Awareness of this ratio allows you to make educated choices regarding your health insurance. It also guarantees that the money you have worked hard for is utilized effectively.

Let’s discuss the medical loss ratio further.

First…

Definition: The Medical Loss Ratio (MLR) is a measure used in the health insurance industry. It represents the percentage of premium revenues spent on clinical services and quality improvement. For example, an MLR of 80% means that 80% of premiums are used for patient care. 20% covers administrative costs and profits.

MLR ensures that insurers put patient care ahead of profits. The Affordable Care Act (ACA) mandates that insurers meet minimum MLR standards of 80% for individual and small group markets, and 85% for large group markets. If insurers don’t meet these thresholds, they must issue rebates to policyholders. This approach is designed to deliver better value and manage healthcare costs. To truly grasp its impact, integrating consumer research and customer experience measures can reveal how these standards shape customer satisfaction and enhance the overall healthcare experience.

The medical loss ratio (MLR) is more than just a number. It’s a crucial part of how health insurance works to benefit you. Here’s why it is important:

Understanding the rules around the medical loss ratio (MLR) is vital. It can give you a clearer picture of how your health insurance premiums are used. Here’s a breakdown of these important rules:

To calculate the Medical Loss Ratio (MLR), follow these steps:

A good medical loss ratio (MLR) is determined by regulations and norms within the industry. In the US, health insurance companies under ACA must maintain a minimum MLR of 80% for individual and small group markets. For large group markets, they must maintain a minimum of 85%. Achieving or surpassing these benchmarks is typically viewed positively. Why? It shows that much of the premium revenue goes toward medical care and quality improvement efforts.

Yet, what constitutes a “good” MLR can differ depending on variables like:

Sometimes, an insurer’s MLR can exceed the regulatory threshold. This may signal that they are making a significant investment in healthcare services and quality enhancement. It could be seen as a positive by policyholders and regulators.

In the end, the effectiveness of an MLR relies on multiple factors. Therefore, it is crucial to consider the wider context when evaluating its importance.

Are you struggling to make sense of heaps of medical loss ratio data? Join the club. Analyzing complex data with Pyramid charts can feel like decoding a cryptic message.

What about Excel? While great for numbers, it falls short in turning data into engaging visuals that tell a story.

But fear not. ChartExpo is your ally in transforming mundane data into captivating visual storytelling. With ChartExpo, you can bid farewell to dull Excel charts and embrace a new era of dynamic, insightful data visualizations.

Let’s learn how to install ChartExpo in Excel.

ChartExpo charts are available both in Google Sheets and Microsoft Excel. Please use the following CTAs to install the tool of your choice and create beautiful visualizations with a few clicks in your favorite tool.

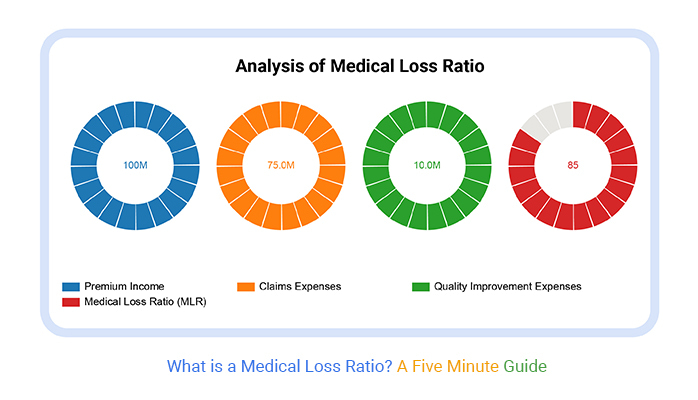

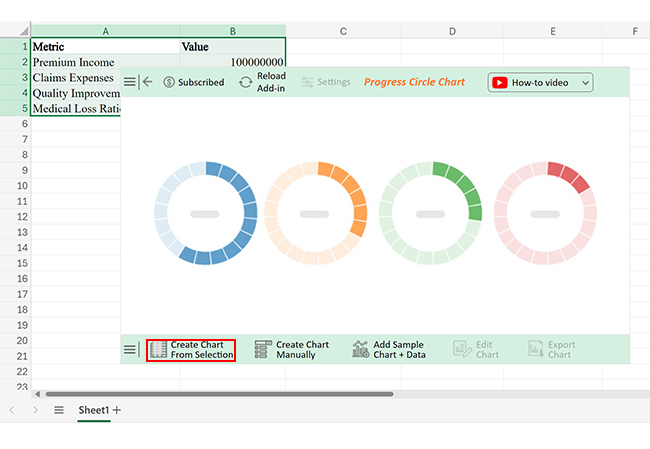

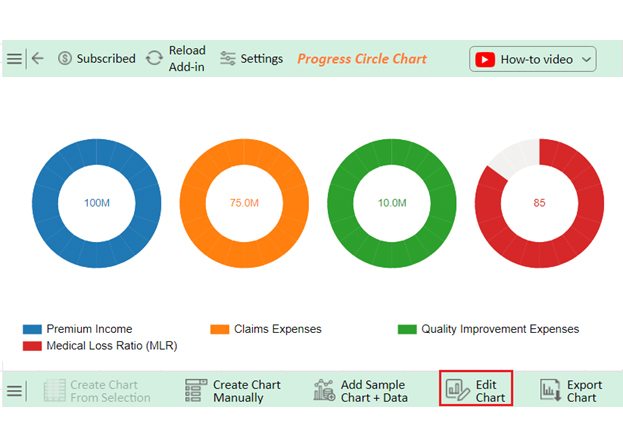

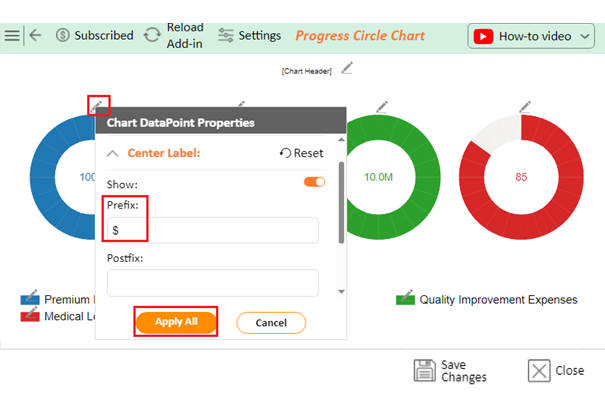

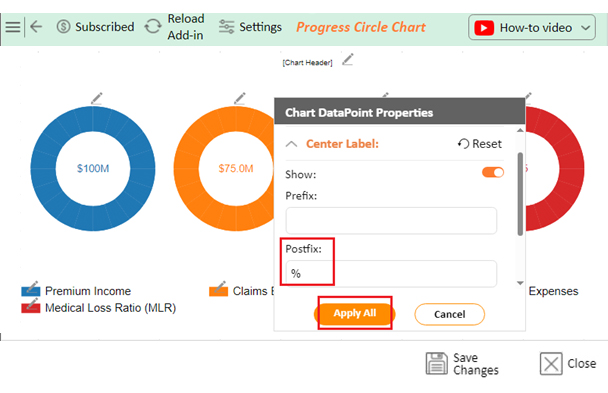

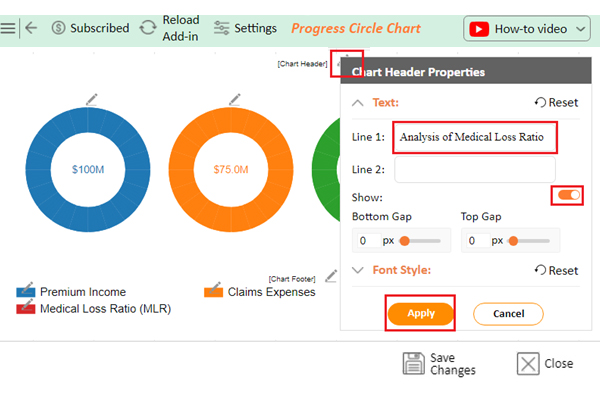

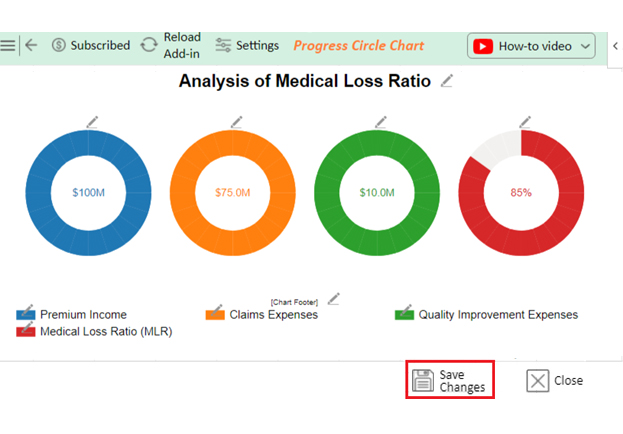

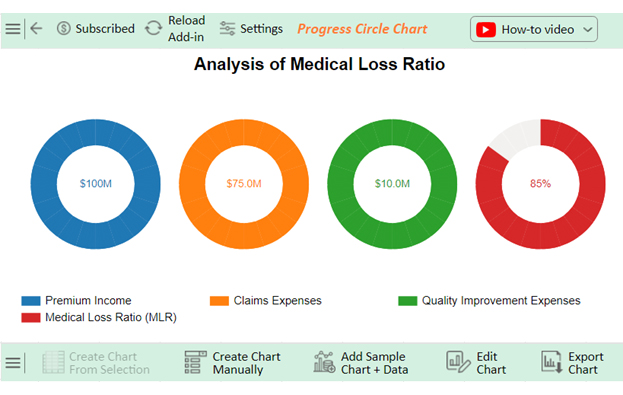

Let’s analyze the medical loss ratio data below using ChartExpo.

| Metric | Value |

| Premium Income | 100000000 |

| Claims Expenses | 75000000 |

| Quality Improvement Expenses | 10000000 |

| Medical Loss Ratio (MLR) | 85 |

The MLR stands at 85%, showing that 85% of premium revenue goes towards claims and improving quality. This indicates effective utilization of funds while adhering to standard regulatory requirements for insurer performance.

The medical loss ratio (MLR) KPI measures the percentage of premium revenues spent on medical care and quality improvements. It ensures insurers allocate funds primarily for patient care, maintaining value for policyholders and compliance with regulatory standards.

The ideal MLR is 80% for individual and small group markets and 85% for large group markets. These benchmarks ensure insurers spend a significant portion of premiums on medical care and quality improvement.

The medical loss ratio (MLR) is a key measure in the health insurance industry. It determines the percentage of premium revenue spent on patient care and quality improvement. This ratio is crucial for ensuring your premiums are used effectively.

MLR rules set specific thresholds. For individual and small group markets, insurers must spend at least 80% of premiums on healthcare. For large group markets, this threshold is 85%. These standards help prioritize patient care over administrative costs and profits.

To calculate MLR, you divide the funds spent on clinical services and quality improvement by the total premium revenue minus certain taxes and fees. This precise calculation ensures fairness and accuracy. Insurers must report this data annually, promoting transparency.

If insurers fail to meet these thresholds, they must provide rebates to policyholders. These rebates ensure consumers receive value for their premiums. For example, if an insurer’s MLR is 75% in the individual market, they must rebate the difference to reach 80%.

There are some exemptions and adjustments to MLR rules. New health plans may be exempt for a limited time. States can request adjustments to prevent market destabilization. These provisions offer flexibility while maintaining consumer protection.

In conclusion, the MLR is vital for safeguarding your healthcare dollars. It ensures a significant portion of premiums is spent on medical care and quality improvement. Understanding MLR rules, calculations, and thresholds helps you make informed choices and get the most from your health insurance.

How much did you enjoy this article?

Calculate accounts receivable turnover ratio to measure credit collection speed, improve cash flow, and strengthen your financial strategy. Read on!

Change Management KPIs are the key to tracking adoption, performance, and ROI during transitions. Find out which metrics matter. Read on!

Data collection methods and techniques determine the quality of every insight you act on. Explore key approaches for gathering reliable data. Read on!