Categories

Margins can flip when claim frequency rises a fraction. Analytics in the insurance industry helps insurers spot those shifts early, before loss ratio reports arrive. It connects policy, claims, and service activity into shared measures.

When underwriting and claims teams trust the same numbers, pricing, and triage decisions move faster.

This guide breaks down definitions, benefits, limits, and common use cases. You will also follow a Power BI walkthrough that keeps the list structure intact.

Along the way, you will see how visuals can present risk, fraud, and renewal patterns without forcing readers into spreadsheets. Use it to plan data work that supports decisions, not slides.

Definition: Analytics in insurance industry is the practice of turning policy, claims, and customer records into repeatable decisions. Teams clean data, define measures, and apply statistical models to score risk and flag anomalies.

Outputs guide underwriting, pricing, reserving, fraud review, and service, so actions follow evidence rather than gut feel. It also standardizes definitions across departments, which makes performance comparisons consistent.

With aligned definitions, analysts can compare results by product, region, and channel without arguing about sources. They can test whether a rule change reduces leakage, measure adjuster workload, and monitor renewal signals. Leaders get dashboards and alerts that surface exceptions early, not after losses compound over time.

It matters because business analytics turns scattered operations data into consistent signals that support defensible decisions across teams.

Key reasons insurers rely on it:

Analytics in insurance industry supports underwriting, claims, fraud, pricing, and retention with shared measures.

Common uses include:

Data analytics in insurance industry is shifting toward cloud pipelines, self-serve dashboards, and model monitoring that shortens decision cycles today.

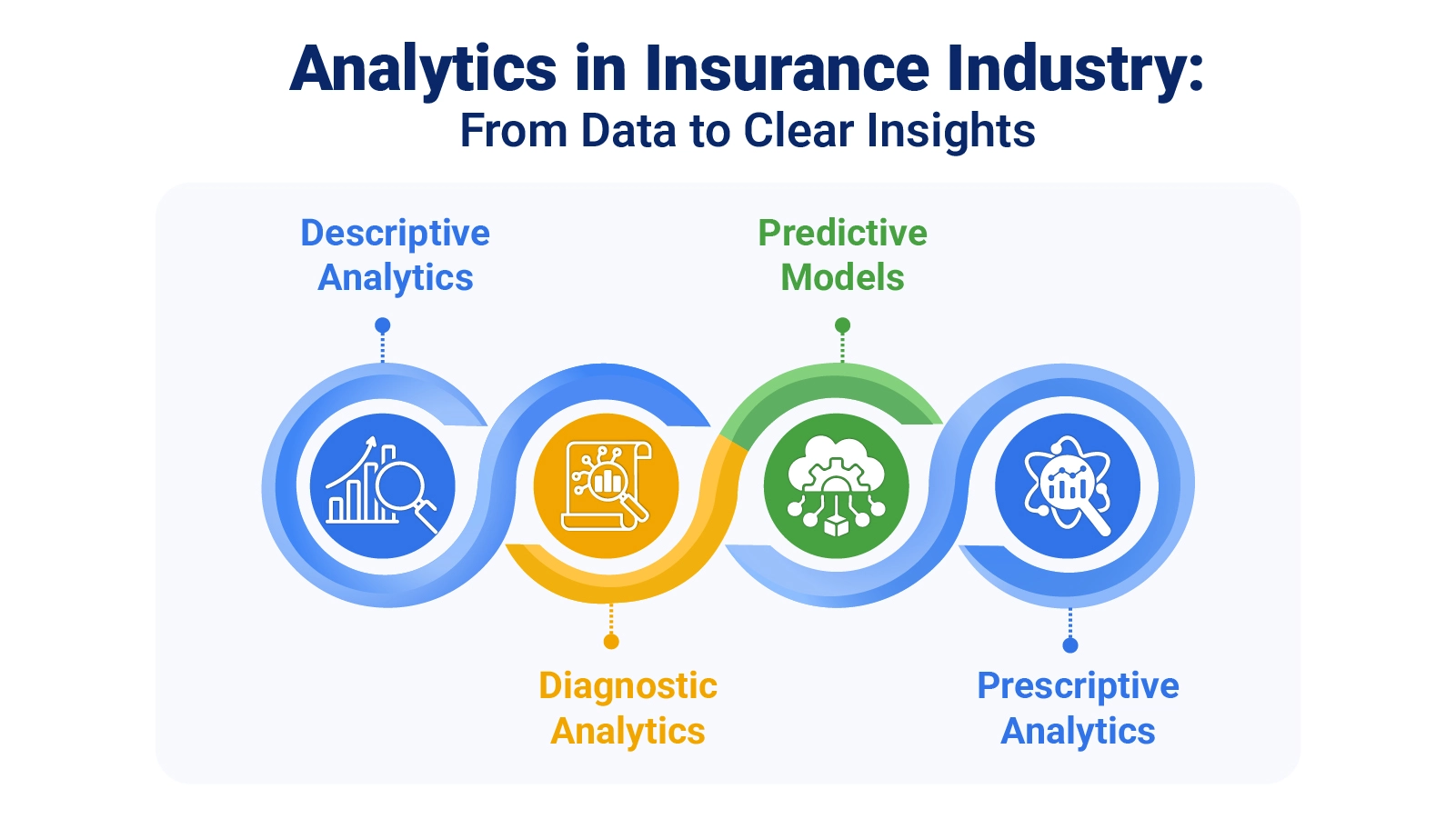

Analytics in insurance industry uses descriptive, diagnostic, predictive, and prescriptive approaches. Each method answers a question, and data analysis stays consistent across underwriting, claims, and retention workstreams.

Examples show how analytics in insurance industry turns raw operations data into dashboards that highlight risk, fraud, and renewal movement.

It tracks intake, routing, approvals, and investigations, letting managers spot bottlenecks and match adjuster capacity to weekly demand across teams.

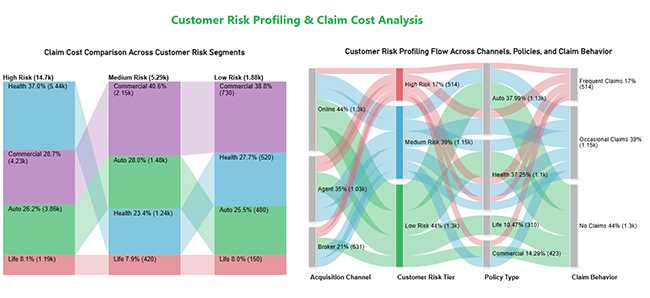

This view compares segments by expected loss and claim cost, helping teams adjust terms and focus outreach on safer cohorts.

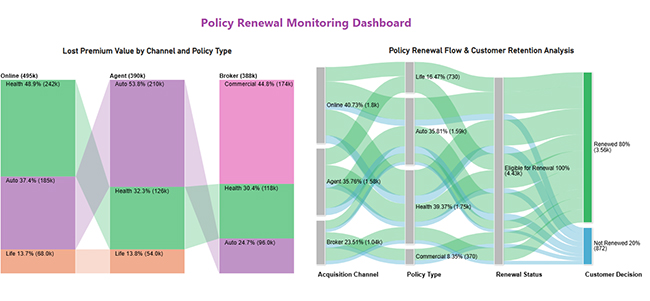

It monitors renewals by channel and product, isolates where premium drops concentrate, and flags cohorts likely to lapse before billing closes, enabling targeted retention outreach early.

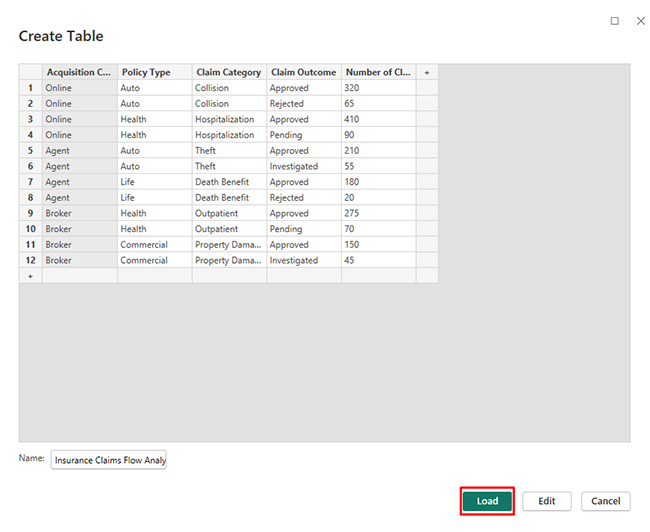

A Power BI workflow starts with inputs, measures, and visuals. Analytics in insurance industry stays usable when refreshed, and definitions remain stable.

First, confirm each data source in Power BI points to claims, policies, and payments, then refresh and validate totals today.

Standardize fields, fix blanks, and align dates so measures calculate correctly everywhere.

Choose KPIs such as loss ratio, severity, frequency, and cycle time, and document formulas to reuse.

Pick visuals that show bottlenecks, segment shifts, and hotspots at a glance.

Use the percentage of total in Power BI to show the product’s share of premium and claims.

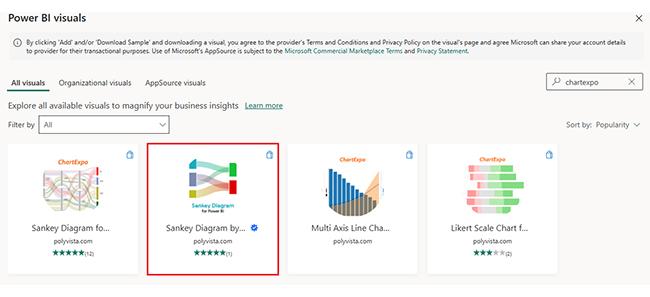

ChartExpo adds Power BI charts that clarify flows, comparisons, and sentiment for stakeholders fast.

Why use ChartExpo?

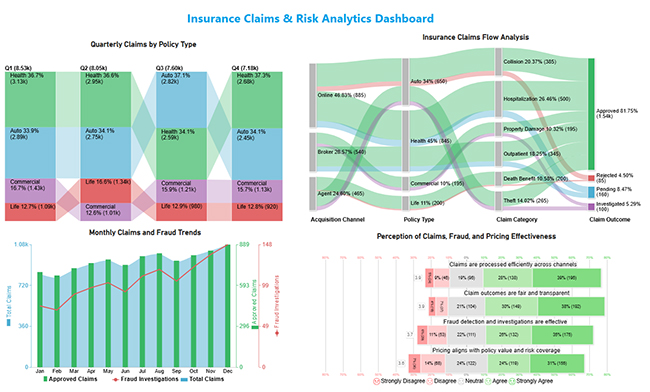

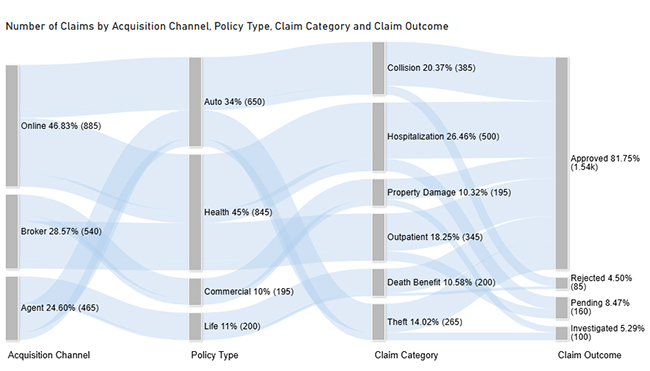

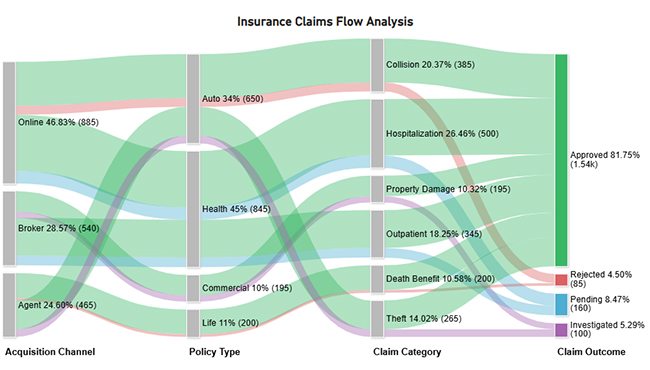

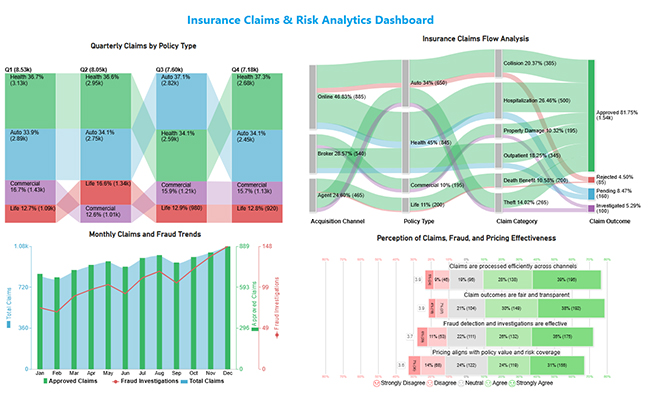

Use this data to build a Sankey Chart now.

|

Acquisition channel |

Policy type | Claim category | Claim outcome |

Number of claims |

| Online | Auto | Collision | Approved | 320 |

| Online | Auto | Collision | Rejected | 65 |

| Online | Health | Hospitalization | Approved | 410 |

| Online | Health | Hospitalization | Pending | 90 |

| Agent | Auto | Theft | Approved | 210 |

| Agent | Auto | Theft | Investigated | 55 |

| Agent | Life | Death benefit | Approved | 180 |

| Agent | Life | Death benefit | Rejected | 20 |

| Broker | Health | Outpatient | Approved | 275 |

| Broker | Health | Outpatient | Pending | 70 |

| Broker | Commercial | Property damage | Approved | 150 |

| Broker | Commercial | Property damage | Investigated | 45 |

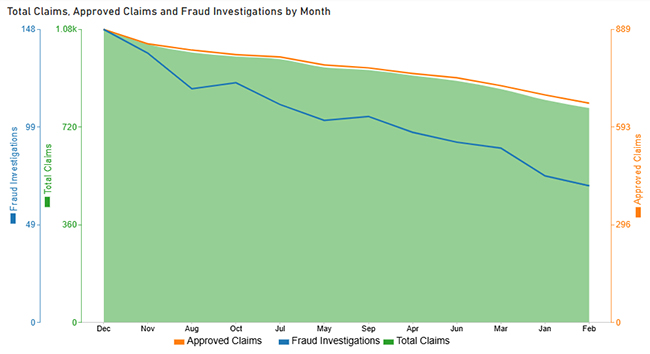

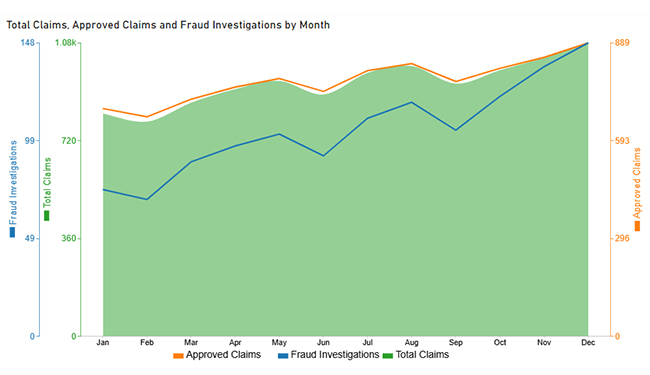

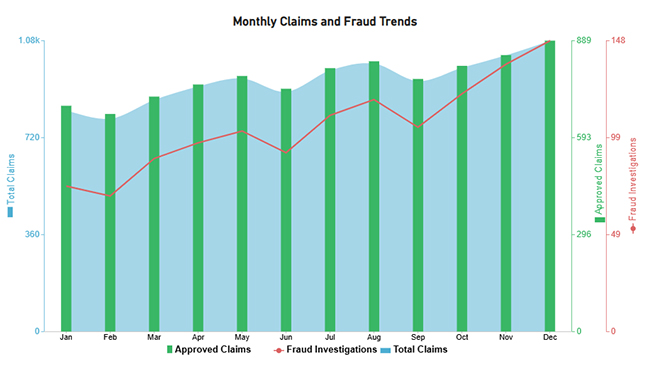

Next, use this table to create a Multi Axis Line Chart for claim trends.

|

Month |

Total claims | Approved claims |

Fraud investigations |

| Jan | 820 | 690 | 74 |

| Feb | 790 | 665 | 69 |

| Mar | 860 | 718 | 88 |

| Apr | 910 | 755 | 96 |

| May | 940 | 781 | 102 |

| Jun | 890 | 742 | 91 |

| Jul | 970 | 805 | 110 |

| Aug | 995 | 826 | 118 |

| Sep | 930 | 772 | 104 |

| Oct | 980 | 812 | 121 |

| Nov | 1,025 | 845 | 136 |

| Dec | 1,080 | 889 | 148 |

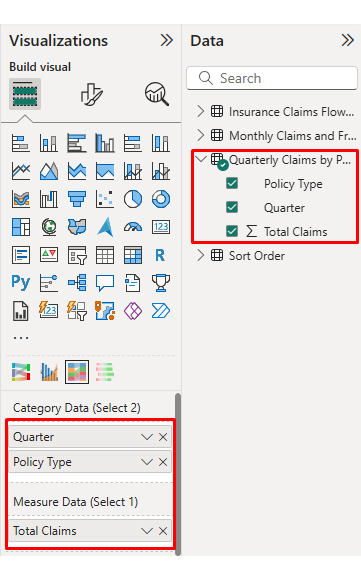

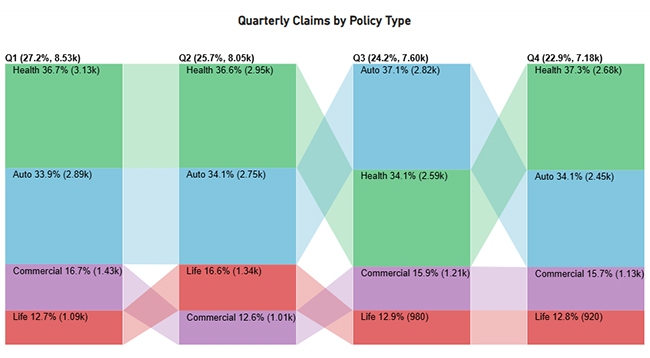

Then, use a table to create a Comparison Bar Chart that contrasts policy types.

|

Quarter |

Policy type |

Total claims |

| Q1 | Auto | 2890 |

| Q1 | Health | 3,125 |

| Q1 | Life | 1,085 |

| Q1 | Commercial | 1,425 |

| Q2 | Auto | 2745 |

| Q2 | Health | 2950 |

| Q2 | Life | 1340 |

| Q2 | Commercial | 1015 |

| Q3 | Auto | 2815 |

| Q3 | Health | 2590 |

| Q3 | Life | 980 |

| Q3 | Commercial | 1210 |

| Q4 | Auto | 2450 |

| Q4 | Health | 2680 |

| Q4 | Life | 920 |

| Q4 | Commercial | 1130 |

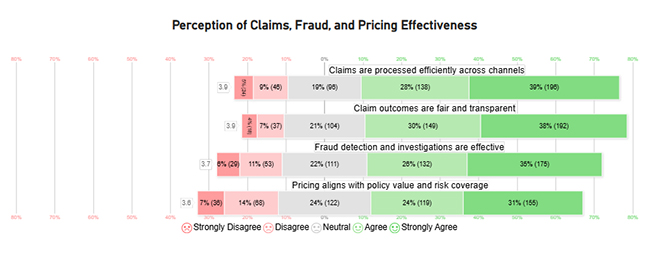

Finally, use this table to create a Likert Chart for survey ratings.

|

Question |

Scale |

Responses |

| Claims are processed efficiently across channels | 1 | 24 |

| Claims are processed efficiently across channels | 2 | 46 |

| Claims are processed efficiently across channels | 3 | 96 |

| Claims are processed efficiently across channels | 4 | 138 |

| Claims are processed efficiently across channels | 5 | 196 |

| Claim outcomes are fair and transparent | 1 | 18 |

| Claim outcomes are fair and transparent | 2 | 37 |

| Claim outcomes are fair and transparent | 3 | 104 |

| Claim outcomes are fair and transparent | 4 | 149 |

| Claim outcomes are fair and transparent | 5 | 192 |

| Fraud detection and investigations are effective | 1 | 29 |

| Fraud detection and investigations are effective | 2 | 53 |

| Fraud detection and investigations are effective | 3 | 111 |

| Fraud detection and investigations are effective | 4 | 132 |

| Fraud detection and investigations are effective | 5 | 175 |

| Pricing aligns with policy value and risk coverage | 1 | 36 |

| Pricing aligns with policy value and risk coverage | 2 | 68 |

| Pricing aligns with policy value and risk coverage | 3 | 122 |

| Pricing aligns with policy value and risk coverage | 4 | 119 |

| Pricing aligns with policy value and risk coverage | 5 | 155 |

Place visuals in a clean grid, add slicers for policy and time, and confirm tooltips work before sharing internally with core teams.

Analytics in insurance industry benefits from insurance data analytics, making underwriting, claims, and service measurable and repeatable.

Insurance data analytics can stall when controls and skills do not align.

Data analytics in the insurance industry helps when models guide pricing, triage, retention, and fraud.

It supports underwriting, claims triage, fraud review, pricing, and service, using shared definitions so teams measure performance consistently across lines of business.

The goal is to reduce uncertainty, select profitable risk, and act faster, while keeping assumptions traceable for audits and regulators.

Yes. Start with one use case, automate refreshes, and standardize metrics, then expand as results fund the next step without large teams.

Analytics in insurance industry delivers value when definitions are governed, and teams act on metrics, not screenshots. Start with a short list of measures for pricing, claims cycle time, and renewal risk. Automate refreshes, add alerts for exceptions, and keep assumptions documented. That foundation makes models safer to scale across products.

Use the earlier sections to pick the next upgrade: cleaner capture, stronger integration, or clearer visuals. Power BI can handle the core workflow, and add-ins help when the default charts limit communication. Tie each dashboard to an owner, a decision, and a follow-up step. That is how analytics becomes operations.

How much did you enjoy this article?

Calculate accounts receivable turnover ratio to measure credit collection speed, improve cash flow, and strengthen your financial strategy. Read on!

Change Management KPIs are the key to tracking adoption, performance, and ROI during transitions. Find out which metrics matter. Read on!

Data collection methods and techniques determine the quality of every insight you act on. Explore key approaches for gathering reliable data. Read on!